Software is simultaneously a production input, a legal subject matter and a tradeable service. This study maps how New Zealand’s IP framework and its GATS commitments interact for computer and related services — and where that interaction creates friction for cross-border supply.

1. Software in New Zealand’s economy

New Zealand’s technology sector has grown steadily over the past decade. In 2025 computer services represented 5.2% of total services exports and 12.5% of total services imports,[1] while the software-as-a-service (SaaS) segment was growing at 16–19% annually since the early 2020s.[2] In that context, software enables other industries but also is a primary export in its own right.

Unlike most other industries in New Zealand — where trade marks and confidentiality agreements share the lead — the computer systems design sector places significant weight on copyright as well. Patents, by contrast, are marginal. This reflects the structure of New Zealand’s IP framework: software is not eligible for patent protection as such,[3] and the skill-and-labour copyright standard protects functional code without requiring inventiveness. In that environment, confidentiality and lead time are rational complements to copyright, rather than substitutes for a stronger formal IP stack.[4]

The time series indicates path dependence in software-sector protection strategy: firms consistently combine copyright with contractual controls rather than patenting. That pattern matters for trade analysis because market entry and expansion often depend less on formal patent positions than on access to code, data and licensing terms in New Zealand. This same structure is visualised in the Toolkit map below.

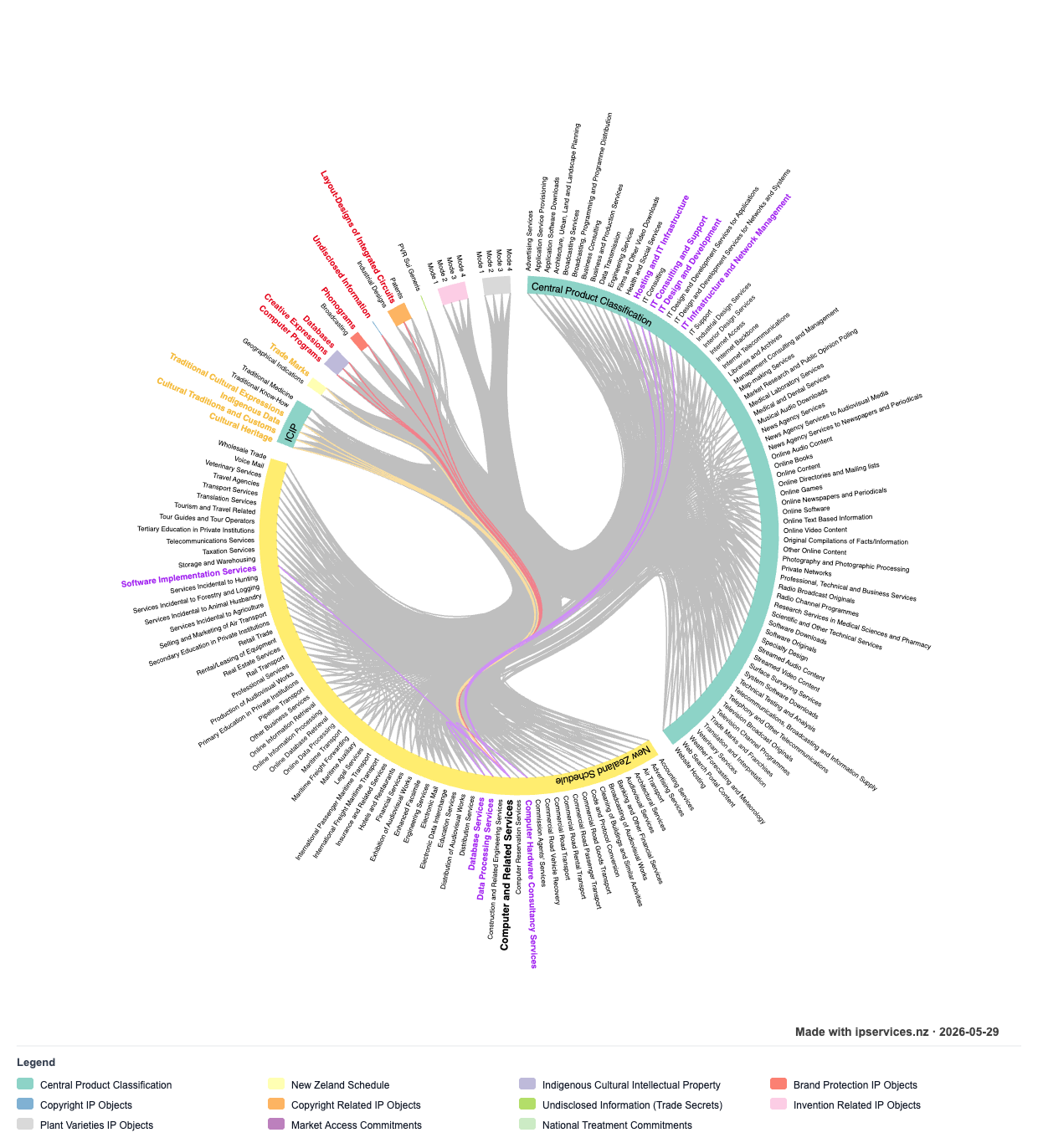

2. What the IP–Services Toolkit shows

The IP–Services Toolkit shows computer and related services — 1(a)–(d) — anchored most strongly to computer programs, databases and undisclosed information (trade secrets). It also retains a thinner but policy-relevant linkage to invention-related IP objects, including patents. Even though New Zealand excludes computer programs "as such" from patentability, patent positions in other jurisdictions and in software-adjacent inventions (implemented methods, hardware-software systems, and platform technologies) can still shape cross-border licensing and market entry conditions.

The CPC ring shows how this stack threads outward to adjacent sectors — IT consulting, architecture and engineering — that depend on the same software inputs. The dependencies run in both directions: software supply requires that the software and related technologies can be licensed and deployed, and that the platform environment is accessible. Neither is guaranteed by the GATS schedule alone.

Important to note, the set of visible linkages could be easily expanded further because computer services are not only a standalone scheduled sector, but a backbone input across many others, similar to financial services.

Against that background, the enquiry should go beyond the question whether computer services are linked to IP. It should focus on which parts of the interface between IP and services shape cross-border supply in practice. The next section therefore focuses on three interface layers where legal design and market operation most clearly intersect.

3. Interface Layers

Three features of New Zealand’s IP framework are most consequential for cross-border supply of computer and software-related services.They work as an interface: first, what the law protects and how protection differs across jurisdictions; second, whether the licences needed to deliver a service can actually be used in the destination market; and third, how exceptions shape what suppliers and users can do once the service is supplied. Taken together, these layers determine whether a scheduled market opening becomes operational in practice.

3.1 Copyright availability and the database gap

New Zealand’s copyright protection for software is comprehensive. There is no minimum inventiveness threshold — skill and labour in creating the work is sufficient — so even routine functional code is protected. That is broadly trade-friendly for inbound services.

The database issue is more specific. New Zealand can protect database compilations through copyright under its originality standard, but it does not provide a standalone sui generis anti-extraction right for substantial investment in non-original databases. Several major trading partners — EU member states in particular — do provide that additional layer.[5] This creates an outbound mismatch. New Zealand's suppliers may face a licensing environment abroad built around stronger database-control rights, while relying at home on copyright and contract for protection of the same asset class.

There is also a cross-jurisdiction originality asymmetry in both directions. Some outputs protected in New Zealand under a skill-and-labour standard may receive narrower or no copyright protection in jurisdictions applying a minimum-creativity threshold. Conversely, material that may sit outside protection in another market can become protected when supplied into New Zealand under New Zealand's threshold and doctrinal framing.

Therefore, the core problem lies in asymmetry of protection and the resulting uncertainty for both suppliers and buyers, rather than in the simple presence or absence of IP protection. The same output can move from under-protection to over-protection (or vice versa) when it crosses jurisdictions, creating bidirectional risk in licensing, infringement exposure and enforcement leverage. In practical terms, this increases clearance costs, complicates contract drafting and raises transaction costs for cross-border software and data services.

3.2 Licensing mechanics as the real binding constraint

New Zealand’s schedule for computer and related services imposes no limitations on Mode 1, Mode 2 or Mode 3; Mode 4 is listed separately with its own conditions. That is a fully open commitment for the first three modes. However, the binding constraint on cross-border supply often lies in the operability of upstream IP licensing.[6]

A New Zealand vendor supplying SaaS to a foreign business customer under the GATS typically relies on licensed frameworks, licensed APIs, licensed middleware and libraries, and delivers to licensed operating environments. If any upstream licence is restricted by territory — or if a foreign regulatory approval requires local hosting — the Mode 1 supply can be blocked without any formal limitation appearing in the schedule at all.

For New Zealand exporters, this means legal predictability is destination-specific: two markets may both appear open at schedule level while diverging sharply in licensing practice, data-governance approvals and enforceability conditions for software-delivery contracts.[7]

This is the core insight from the framework developed in Part III: services supply operates through an IP layer, and the operability of that layer — the ability to obtain and exercise the relevant licences — is as decisive as the scope of the services commitment itself.

The same pattern appears in broader discussions of innovation policy. Technology-transfer outcomes depend less on formal entitlement design alone and more on whether institutions make practical licensing and deployment pathways work across borders.[8]

3.3 Exceptions for digital delivery

New Zealand applies a relatively narrow exceptions model for copyright compared with several competitor jurisdictions. In practical terms, some secondary and data-processing uses that may proceed more easily elsewhere can require additional licensing and clearance in New Zealand.

For New Zealand developers, this can increase compliance cost and slow product iteration. For foreign suppliers serving New Zealand customers, routine technical acts in digital delivery still need a clear legal basis, which can make deployment and contracting more complex.[9]

The effects are cumulative across the software lifecycle. At the design stage, firms must narrow or restructure features to avoid legal uncertainty. At the delivery stage, additional permissions and contractual safeguards become necessary. At the post-sale stage, updates, interoperability fixes, and model improvements can all carry extra transaction cost because each step requires legal validation.

The same dynamic appears with technical access controls. Where software is supplied through controlled platforms, limits on permitted workarounds can reduce what buyers can do in practice, especially in cloud settings where users do not control the underlying code or infrastructure.[10]

From a trade perspective, this does not usually block market entry in a formal sense; instead, it changes the economics of supply. Suppliers with larger legal and compliance capacity absorb these frictions more easily, while smaller firms face proportionally higher costs. The result can be weaker competitive pressure and fewer options for users, even in sectors that look open at schedule level.

4. Takeaway

New Zealand’s scheduled commitments for computer and related services are broadly liberal. The friction is not in the schedule. It lies in whether IP licences can be obtained and exercised across borders, in the regulatory asymmetry between New Zealand and trading partners, and in the scope of exceptions that shape what buyers and developers can legitimately do once software is supplied.

In short, openness into New Zealand and export success for New Zealand suppliers are both controlled less by headline commitments than by whether destination IP and data conditions make cross-border software supply operational in practice.

Coherent trade policy means attending to those upstream and downstream layers — not just to the schedule. For an analysis of how analogous dynamics play out in audiovisual and streaming services, see Study 2.

Statistics New Zealand International Trade Dashboard (year ended December 2025, rest of the world, services and computer services series) https://statisticsnz.shinyapps.io/trade_dashboard/. ↩︎

NZTech and Ministry of Business, Innovation and Employment New Zealand SaaS Sector Insights (Wellington, 2023) at 16. ↩︎

Patents Act 2013 (NZ), s 11(1)(b) [Patents Act] (computer programs "as such" excluded from patentability); Copyright Act 1994 (NZ), s 14. ↩︎

Statistics New Zealand "Business Operations Survey — IP protection strategies by industry" table BUO021AA (last updated 25 March 2022) https://infoshare.stats.govt.nz. ↩︎

Directive 96/9/EC of the European Parliament and of the Council on the legal protection of databases [1996] OJ L77/20 [Database Directive], art 7 (sui generis right protecting substantial investment in obtaining, verifying or presenting data). ↩︎

Nikita Melashchenko "Two Regimes, One Market: IP–Services Linkages and New Zealand's Trade Policy" (2025) 56 VUWLR (preprint available at https://doi.org/10.25455/wgtn.31062634), Part IV.A. ↩︎

Susy Frankel "International Intellectual Property, Innovation, Technology Transfer and Sustainable Development" in Christophe Geiger (ed) Intellectual Property, Ethical Innovation and Sustainability: Towards a New Social Contract for the Digital Economy (Edward Elgar, 2025) preprint available at https://dx.doi.org/10.2139/ssrn.5513818. ↩︎

Melashchenko, above n 6. ↩︎

Melashchenko, above n 6. ↩︎

Melashchenko, above n 6. ↩︎